Fun and Easy Ways to Remember the Accounting Equation

A lot of new accountants and bookkeepers nowadays are coming into the profession without a thorough understanding of how the five major types of accounts in accounting relate to each other and also how debit and credit affect these accounts.

This is incredible...

We are talking about the so called professionals of our industry. And this isn't even considering business owners who run their own books without any formal training.

At any point of time, you should be able to produce correct journaling. For example, something simple, business is paying $2,000 monthly rent from their bank account: you Credit Assets accounts (bank balance) $2,000 and Debit $2,000 for the rent expense.

Since the first double entry bookkeeping theory book published by Luca Pacioli in 1494, debits and credits are behind most cultural and absolutely all economic advances. But...

The struggle for some students and professionals is real.

For years I have been on a mission to help them and find the best methods to memorise Debits and Credits for the future generation.

Let's put an end to this struggle right now.

I have been asking my colleagues: "What method are you using to remember debits and credits? "

We are all different and require methods that would work for us, personally.

This article is a collection of the 3 best methods to remember debits and credits.

If you're anything like me, there's only one frustration that comes with learning a new skill.

You want things to be perfect… instantly!

Seriously – who doesn't?

These methods help you get it right 100% of the time.

And the top 3 winners are:

- Hands Method

- DC ADE LER Method

- BS and P&L Method

How to Choose the Best Method to Remember Debits and Credits

We are all humans (hopefully) and we are all different, depending on your natural learning predisposition:

- Are you predominantly visual?

- Are you predominantly auditory?

- Are you predominantly kinesthetic?

It does not really matter!

Each of these methods have elements of all of them.

The secret is…

Just read all of them and you will instantly feel the one that resonates with you naturally, this would be the one to choose.

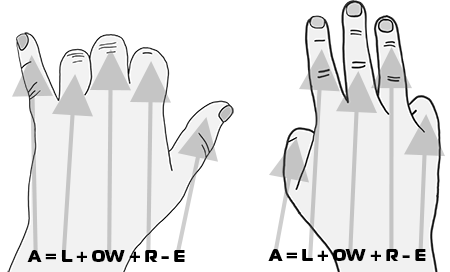

Method 1: Hands Method

This method helped hundreds of thousands of accountants and bookkeepers all around the world. In my experience this is by far the most popular method.

Feel free to skip the following paragraph, as it is a derivation of the method from the classic accounting equation.

Let's start with the basic accounting equation: Assets = Liabilities + Owners' Equity (A = L + OE).

The next step is to define Owners' Equity: Owners' Equity = Beginning Owners' Equity + Net Income (OE = BOE + NI)

Then, what is Net Income? Net Income = Revenues - Expenses (NI = R - E)

Finally, you can expand the basic accounting equation to: Assets = Liabilities + Owners' Equity + Revenues - Expenses (A = L + OE + R - E)

This final equation includes the 5 main types of accounts in accounting as variables.

- Assets

- Liabilities

- Owners' Equity

- Revenue

- Expenses

Imagine them as five fingers on your hand.

Left hand - Debit

All what you need to remember is the left hand going up with two fingers (thumb and pinkie) pointing up. Almost like in the rock concert, where fans are screaming: "Debit! Debit! Debit!"

Pinkie - Pointing Up - Debit increases Assets

Ring Finger - Pointing Down - Debit decreases Liabilities

Middle Finger - Pointing Down - Debit decreases Owner's Equity

Index Finger - Pointing Down - Debit decreases Revenue

Thumb - Pointing Up - Debit increases Expenses

Right hand - Credits

Thumb - Pointing Down - Credit decreases Assets

Index Finger - Pointing Up - Credit increases Liabilities

Middle Finger - Pointing Up - Credit increases Owners Equity

Ring Finger - Pointing Up - Credit increases Revenue

Pinkie - Pointing Down - Credit decreases Expenses

| ASSETS | LIABILITIES | EQUITY | REVENUE | EXPENSES | |

| DEBIT | ↑ increase | ↓ decrease | ↓ decrease | ↓ decrease | ↑ increase |

| CREDIT | ↓ decrease | ↑ increase | ↑ increase | ↑ increase | ↓ decrease |

So, every time when you need to remember when to increase revenue, remember your right hand - it is a Credit.

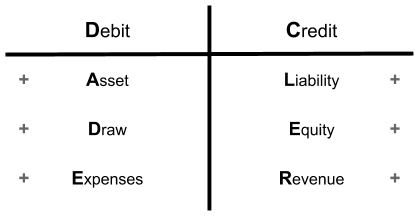

Method 2: DC ADE LER Method

This method has one key advantage among multiple ones I have encountered: it is the easiest to recall when you need it.

In this case, all you need to remember are the 'words' DC ADE LER and then spell them out in the following table. DC are the headers left to right. ADE in the left column and LER in the right.

Debits are always on the left. Credits are always on the right.

Both columns represent positive movements on the account so:

- Debit will increase an asset

- Credit will increase a liability

- Debit will increase a draw

- Credit will increase an equity

- Debit will increase an expense

- Credit will increase a revenue

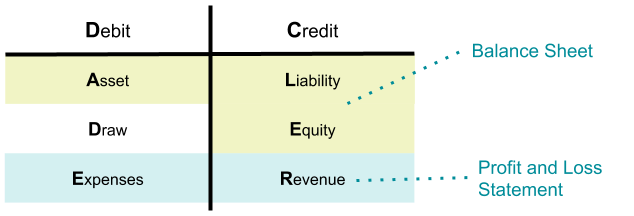

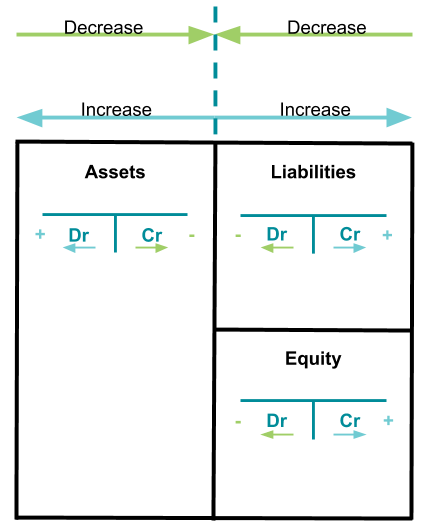

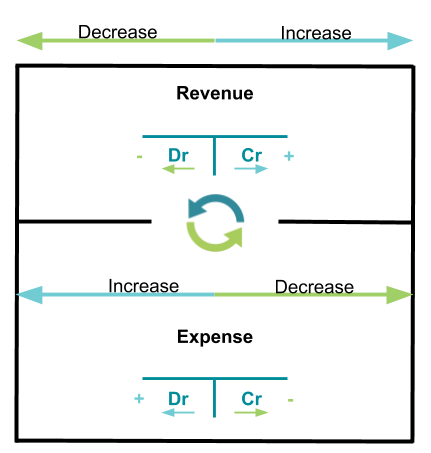

Method 3: BS and P&L Method

This is probably the most comprehensive method. Big advantage of this method is that it leaves no room for an error, as soon as you learn it, you will be able to get it right all the time.

This method utilises your special memory the strongest:

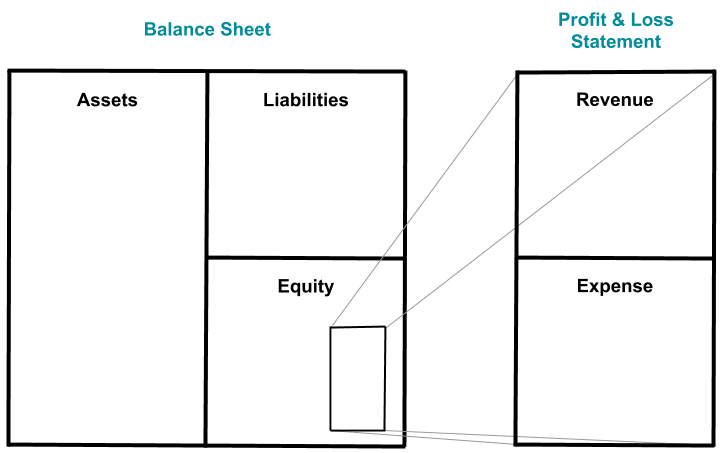

The Image above is very easy to remember. You can clearly see what belongs to:

- Balance Sheet:

- Assets

- Liabilities

- Equity

- Profit and Loss Statement (part of Equity)

- Revenue

- Expenses

The accounts facing the middle are decreasing the account (marked in light green). T-accounts pointing away from the middle are increasing the account (marked blue).

Remember, in Balance Sheet Revenue and Expenses are swopping around roles.

Extra Learning Tips (Revision)

Debits and Credits are neither good or bad, they are not the same as subtracting or adding. They represent the duality of financial transactions, flow of an economic benefit from one side to another.

Another way of looking at it is to see Debit as a destination of an economic benefit and Credit as a source.

Debit (Destination):

- Assets, where entity gains: building, cash and equipment. Destination is an entity that now owns it.

- Expenses, where destinations are a contractor or a supplier, whom the money paid to.

- Dividends, paid out to owners. Destination is an owner.

Credits (Source):

- Assets, where money paid out of a bank account to someone. Bank account is a source of economic benefit.

- Liabilities, where a company is taking a loan. This loan is a source of cash in the bank or new equipment acquired.

- Revenue, is the source of cash in the bank.

Action Points (Revision Exercise)

The best thing that you can do right here, right now is to open balance sheet and profit and loss statements and identify Sources (Credits) and Destinations (Debits) for the following transactions:

- Transferring cash from one bank account to another.

- Receiving money for service provided.

- Paying out a loan.

- Receiving interest on long-term deposit in a bank.

- Paying for a marketing expense.

Conclusion

Not that much has changed in T-Accounts fundamentals described above, since "Particularis de computis et scriptus" ('Particulars of Reckonings and Writings') were published way over 500 years ago.

However, people had more than enough time to perfect the learning techniques. I hope methods described above will help you in your professional life.

Please, try this methods and few months down the track, let me know which one resonates with you the most and why.

If you found this article useful, please make a link to it, it will help other people to find it.

Really looking forward to hearing from you. What method are you using to remember debits and credits? Please post them in the comments.

Subscribe by email and instantly get FREE Illustrated eBook. Adequate 'positive' cash flow is essential for the survival of any business, yet this is something that over 50% of small business owners struggle to manage.

Source: https://avers.com.au/Debit-and-Credit-Rules-T-Accounts/

0 Response to "Fun and Easy Ways to Remember the Accounting Equation"

Post a Comment